How Parametric Climate Insurance Works: A Practical Guide for Businesses and MSMEs

- Arnav Patnaik

- May 11

- 5 min read

India experienced extreme weather on 331 out of 334 days in 2025. That figure comes from the Centre for Science and Environment's Climate India 2025 report, published in December 2025. For businesses and MSMEs, this is not an abstract statistic; it reflects a real and growing operational risk.

This means floods, heatwaves, and unseasonal rain are now near-daily business risks. Most small businesses have no financial shield when the weather shuts them down. Parametric climate insurance is one tool that can change that.

The Problem: Extreme Weather Is Now an Everyday Business Risk

India has over 63 million MSME units employing more than 110 million people. These businesses are among the most exposed to weather extremes. They operate with thin margins and little financial buffer.

For instance, when Cyclone Michaung hit Tamil Nadu in December 2023, it affected 4,800 MSME units spread across 24 industrial estates. Losses reached at least USD 360 million. In fact, in 2025, climate-related disasters cost India an estimated USD 12 billion.

Traditional insurance was never designed for this pace of disruption. Assessors take weeks to visit the site when weather events hit. As a result, the paperwork stretches into months, and the cash flow is already broken, pushing the MSMEs into debt.

What Is Parametric Climate Insurance?

Parametric climate insurance pays out based on a measurable event. Unlike traditional insurance, there is no need for a physical inspection of your losses. The trigger is a number, such as

rainfall exceeding 250 mm in 24 hours,

wind speeds above 90 km/h, or

temperatures crossing 45°C.

To simplify, think of it like a smoke detector. A smoke detector does not wait for the fire brigade to confirm the presence of a fire. It goes off when smoke crosses a threshold. Parametric insurance works the same way. When the weather event exceeds a pre-agreed level, the payout is paid automatically.

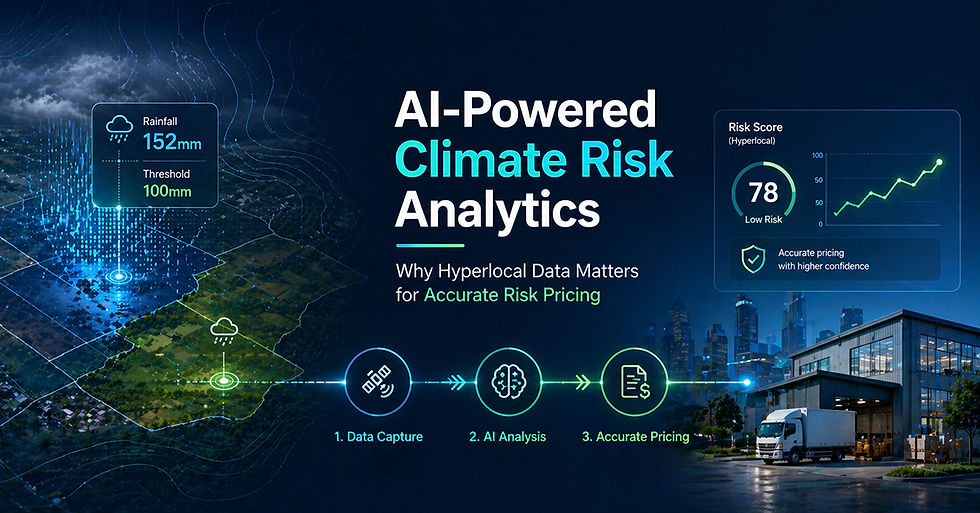

The data for the trigger comes from independent sources, such as the India Meteorological Department (IMD), satellite readings, or weather station networks. Thus, there is no claim to file and no surveyor to wait for.

How It Works for an Indian Business: An Illustrative Scenario

Consider a textile unit in Surat. Surat suffers a high risk of flooding during the monsoon months, June to September. The business owner takes a parametric policy after completing a business climate risk assessment with this trigger: If rainfall in the Surat IMD weather station exceeds 300 mm in any 48-hour period, the policy pays out INR 5 lakh within 72 hours.

In August 2025, rainfall in Surat crosses 320 mm over two days. The IMD data confirms the trigger, which the insurer's system reads automatically. Within three days, the payment arrives in the business owner's account.

This creates a fast, seamless, and simplified process. There is no claim form, assessor visit, or settlement negotiation. The business uses that money to repair machinery, pay workers, or cover lost orders while operations resume.

**Note: This is an illustrative scenario to explain the mechanism. Actual policy terms vary by insurer and product.

Real pilots are already running in India. Nagaland received its first parametric payout for rainfall-triggered flooding under a policy from SBI General Insurance, with Munich Re as reinsurer.

What This Means in Practice for Businesses

Between traditional and parametric insurance, speed is the differentiating factor. Traditional business interruption insurance can take weeks to settle. Parametric payouts for climate risk insurance arrive in days, even hours, after the trigger event is confirmed.

This matters because weather damage is rarely just physical. The real cost is downtime where critical orders are missed, supply chains are broken, and workers are sent home. Fast cash flow allows businesses to restart before the losses compound.

Three practical outcomes businesses can expect from a well-designed parametric climate risk insurance policy:

Liquidity within days of a covered event, not months

No paperwork, no loss surveys, no adjuster visits required

Predictable cover since the trigger and payout are fixed in the contract upfront

Businesses can also stack parametric cover on top of traditional property insurance. Parametric insurance fills the gap between the event and the traditional payout. It does not serve as a replacement, but it complements the gap.

Comparing Traditional Business Insurance and Parametric Climate Insurance

To understand in detail, let’s take a deep dive into how traditional and parametric insurance measure against each other.

How Traditional and Parametric Insurance Differ for MSMEs

In the simplest terms, traditional business insurance pays only after an inspection that verifies that your business has suffered losses. In contrast, parametric climate insurance will pay when the trigger conditions are met, irrespective of whether or not you have suffered losses.

Feature | Traditional Business Insurance | Parametric Climate Insurance |

Payout trigger | Verified physical loss after assessment | Pre-agreed weather data threshold |

Average payout time | Weeks to months | ~ 24 hours of meeting trigger conditions |

Claims process | Surveyor visit, documentation, negotiation | Automatic; no filing required |

Basis of cover | Actual financial loss incurred | Occurrence of the specified event |

Basis risk | Low (loss is directly assessed) | Exists (trigger may not match actual loss) |

Table 1: Comparison of traditional and parametric business insurance.

What Parametric Climate Insurance Does Not Cover

While parametric climate insurance can protect businesses from extreme weather events, they have a significant limitation called basis risk. This is the gap between what the trigger says and what actually happened to your business.

Here is a simple example. A policy pays out when rainfall exceeds 300 mm. Your factory floods badly, but the IMD station nearest you records 285 mm. Since the trigger is not met, the policy does not pay. Your loss is real; however, your insurance policy does not respond.

This is not a flaw unique to India. The World Economic Forum's January 2025 analysis on parametric insurance identifies basis risk as the key structural challenge in any parametric product.

But this does not mean that you should not opt for climate risk insurance. The responsibility falls on you to understand which triggers will impact your business and set the triggers accordingly. This calls for a thorough business climate risk assessment.

Wrapping Up: Where This Leaves Indian Businesses Today

India's climate data tells a clear story. Extreme weather is no longer a rare disruption; it is a recurring operating condition. For businesses and MSMEs, the question is not whether a weather event will disrupt operations, but when.

Parametric climate insurance offers speed and certainty that traditional insurance cannot. It does not remove risk. It does not replace good risk management. But it provides fast, predictable liquidity at the moment businesses need it most.

India's insurance regulator, IRDAI, has signalled the need for broader climate risk cover under its 'Insurance for All by 2047' framework. As the product category matures, businesses that understand how parametric cover works and how it benefits them will be better positioned to manage climate risk.

Ready to Explore Parametric Climate Insurance for Your Business?

Protect your business from extreme weather by exploring what is available in your sector. Check out parametric insurance policies and learn how they can make your business climate resilient.

Frequently Asked Questions

How do businesses decide the right trigger levels for a parametric policy?

Choosing the right trigger depends on historical weather patterns and how those conditions impact operations. Businesses often analyse past disruptions, such as rainfall levels that caused shutdowns, setting thresholds that reflect real financial risk rather than arbitrary numbers.

Can parametric insurance be customised for different industries?

Of course. A textile unit, a logistics company, and a food processing business face very different climate risks. Policies can be structured around specific triggers like rainfall, temperature, or wind speed based on the industry’s exposure.

Is parametric insurance affordable for small businesses?

Costs vary based on risk exposure and payout structure, but parametric climate insurance is often designed to be more accessible than traditional policies, especially for MSMEs that need quick liquidity rather than large indemnity covers.

How do insurers prevent misuse if no loss verification is required?

The system is designed around objective triggers rather than subjective claims. Since payouts depend only on verified data thresholds, there is little room for manipulation or inflated claims in parametric climate insurance.

Comments